Pre-revenue valuation method

Before you raise any money from investors, you need to make sure that the company value can be justified. I know that this is a very difficult task. However, there are several methods to get it done. One of the major problems with all methods is that you need to justify why you are asking for that particular amount of money. I was always skeptical when raising money, and giving up equity if the Startup is your only income. Your company might be super successful but you realize that you have lost equity due to the fact that you needed an investment. My suggestion is that you should not give up your equity at this early stage as you can end up with little stake in your company. Of course, the investors are motivated to leave you enough so you can feel that your all work will be awarded, however, investors might also be very eager to take a big chunk of your company. Once the company has some revenue and you can demonstrate that you have a strong team, market share, revenue, and product, it is far easier to raise money and give up just a little of your company share in exchange for the initial investment. So how do you prepare for the financial projection? Please remember, that every investor would like to know the justification of the amount you are proposing.

Here are three methods I like the most. The fourth method is created by me. 90% of all investments are unsuccessful. Most of the startups go bankrupt. They don’t survive the first year or two years.

Berkus Method

This method is based on 5 elements:

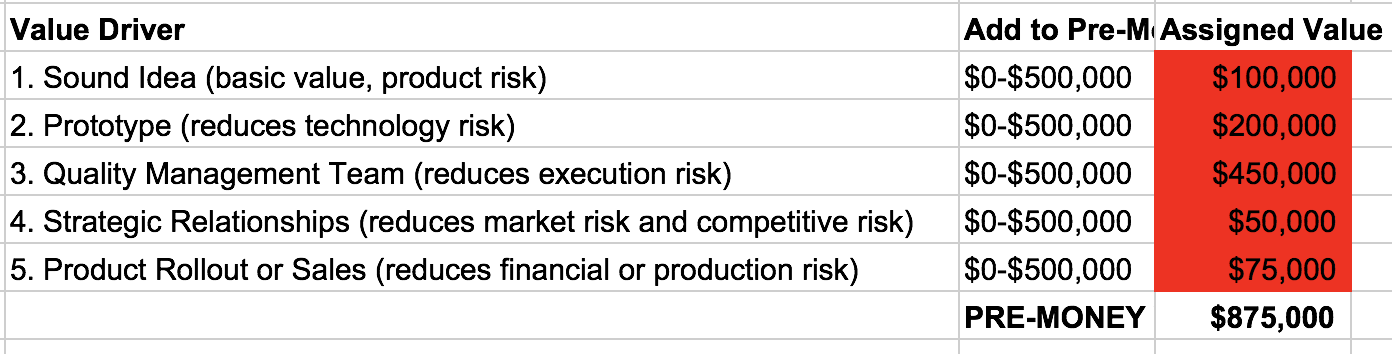

- Sound Idea (basic value, product risk),

- Prototype (reduces technology risk),

- Quality Management Team (reduces execution risk),

- Strategic Relationships (reduces market risk and competitive risk),

- Product Rollout or Sales (reduces financial or production risk)

Each element has a maximum value of $500,000 where you assign the value on your best judgment which can be proved.

For example, your Strategic Relationship with the current client might bring $500,000 net income to the company so you will put $500,000 as this is the real value of your special condition valuing the element on the higher number possible.

If each element earns a maximum valuation of $500,000, you will end up a valuating company of $2,500,000.

In our case, we have valued each element of the company with much lower $$$ as the management or team is the only valued asset, we put the higher value to that element. The total Pre-money is $875,000.

We will offer these tools for free of charge as far as it might increase our traffic and get a few clients to start using our platform. If you look at the There are quite a few competitors who are well established, Every company.

Scorecard Value Method

Scorecard Value Method is mostly used by the Angel Investors.

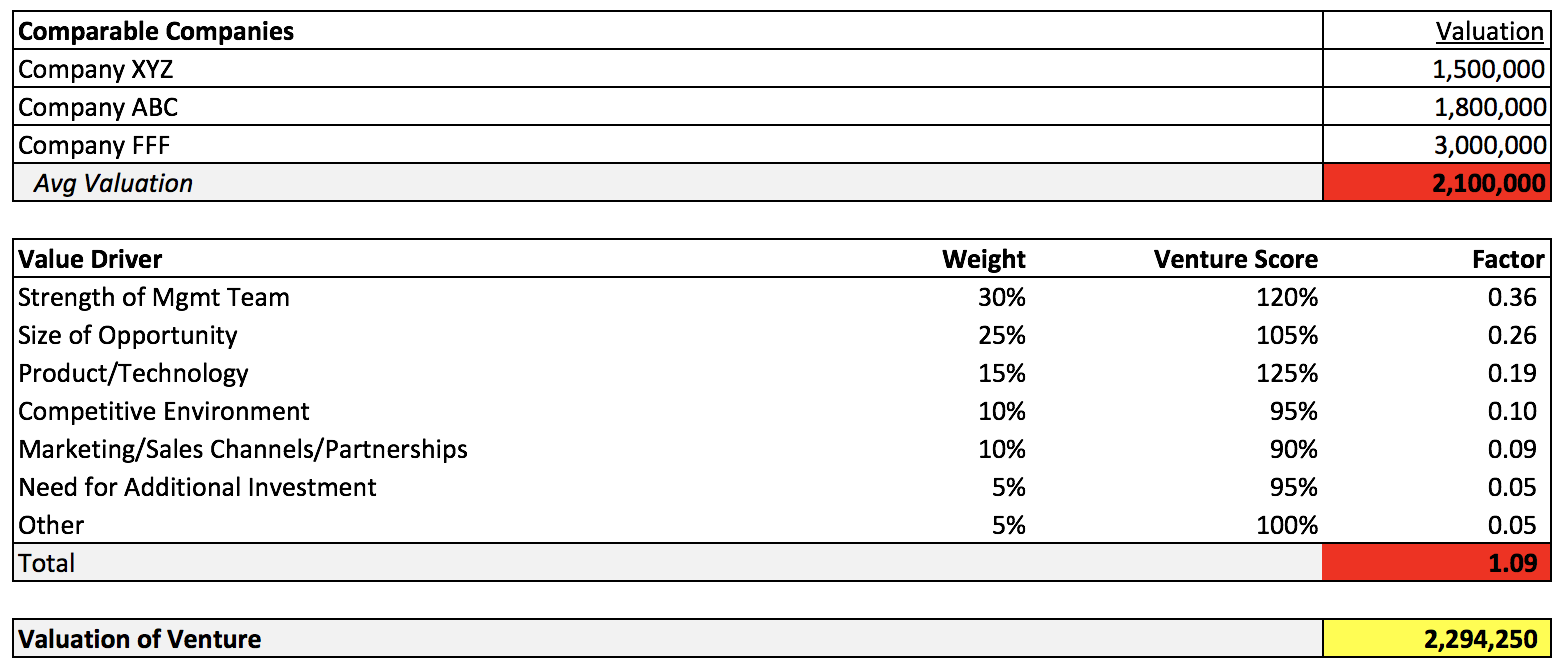

The first thing you need to do, it is to find in your region or market similar company being valuated. You take into account the average value of the investment. You take the Pre-money valuation value.

I would be looking at the Angel list and see what numbers you might fit into.

The second element is to compare the startup to the perception of other startups within the same region using factors such as:

- Strength of the Management Team (0–30%)

- Size of the Opportunity (0–25%)

- Product/Technology (0–15%)

- Competitive Environment (0–10%)

- Marketing/Sales Channels/Partnerships (0–10%)

- Need for Additional Investment (0–5%)

- Other (0–5%)

The ranking of these factors is highly subjective, I have the same problem with this method as with Berkus Method. If the investor will ask you why you have come up with that particular number, you need to be ready to answer that question. It is the same approach as we have with Berkus Method.

Risk Valuation Method

You need to come up with the average value of the similar Startup in your region. We can come up with an example of $1,000,000. Once you have that, you will need to assign a risk factor to each element. Risk factor +2 very positive, +1 positive, 0 neutral, -1 negative and -2 very negative.

The initial pre-money valuation is adjusted positively by $250,000 for every +1 and negatively by -$250,000 for every -1, $500,000 for every +2 and negatively by -$500,000 for every -2. You will minus or plus each value from each other and you will get a number which you will sum up with the averaged value of all similar companies in your area.

- Management

- Stage of the business

- Legislation/Political risk

- Manufacturing risk

- Sales and marketing risk

- Funding/capital raising risk

- Competition risk

- Technology risk

- Litigation risk

- International risk

- Reputation risk

- Potential lucrative exit

Each risk (above) is assessed, as follows:

- +2 very positive for growing the company and executing a wonderful exit

- +1 positive

- 0 neutral

- -1 negative for growing the company and executing a wonderful exit

- -2 very negative

Once you have the above math done based on the values assigned to each element, you will get a result.

By the way, here is the current stage for each investment. Before I moved to the Bay Area, I didn’t know that there is something like Pre-seed. We have just Seed Round in Hong Kong. I guess the Venture Capital environment is very unique compared to any other places in the world.

Here is the table:

- Pre-seed: raising $200K – $500K at a pre-money valuation of $1M – $3M

- Seed: raising $500K – $2.5M at a pre-money valuation of $2M – $6M (expected revenues are $0 – $50K per month)

- Series A: raising $3- $12M at a pre-money valuation of $10M – $40M (expected revenues are $100K – $250K per month)

- Series B: raising $10M – $25M at a pre-money valuation of $30 – $100M (expected revenues are $350K – $800K per month)

- Series C: raising over $20M at pre-money valuations of over $100M (expected revenues are over $1M per month)